If you are feeling buried under a mountain of credit card statements or waking up in a cold sweat over a looming foreclosure notice, you are not alone. In San Diego County, the cost of living and unexpected life events often push families to a breaking point. When you reach that stage, the conversation usually turns to bankruptcy. But which path is right for you?

Choosing between Chapter 7 and Chapter 13 is a bit like choosing between a sprint and a marathon. One gets you to the finish line fast, while the other is a steady, strategic climb toward saving your most valuable assets. As a bankruptcy attorney in El Cajon, CA, we are here to help you pick the right shoes for the journey.

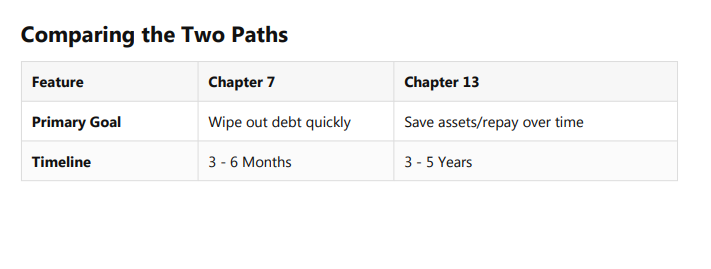

What is Chapter 7 Bankruptcy (The Quick Exit)?

Think of Chapter 7 as the "Quick Exit." It is designed to wipe the slate clean as fast as possible. If you are struggling with medical bills, personal loans, or high credit card interest, this is often the most direct route to a fresh start.

In a Chapter 7 case, you can typically see your qualifying debts discharged (wiped out) in as little as 3 to 6 months. You don't make a payment plan; instead, the court looks at what you own and what you owe. In most consumer cases in San Diego, you won't actually lose your belongings because of the California exemptions we will discuss later.

Do you qualify for the Chapter 7 Means Test?

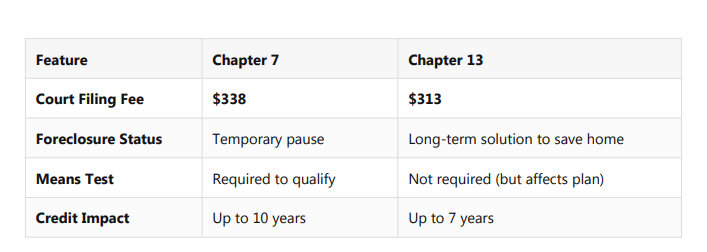

The biggest "if" with Chapter 7 is the Means Test. The court looks at your household income over the last six months and compares it to the median income in California. If you make too much money for your household size, you might be "tested out" of Chapter 7 and pushed toward a Chapter 13 repayment plan.

What is Chapter 13 Bankruptcy (The Reorg)?

While Chapter 7 is a sprint, Chapter 13 bankruptcyis a marathon: but one with a very high prize at the end. It is a reorganization of your debt. You work with your bankruptcy attorney to create a 3-to-5-year payment plan that fits your budget.

Chapter 13 is the "hero" for homeowners. If you have fallen behind on your mortgage and the bank is threatening foreclosure, filing for Chapter 13 can stop the process in its tracks. You can "cure" those missed payments over several years while staying in your home. It’s also an excellent tool if you are behind on car payments and want to prevent a late-night repossession.

Why choose a 5-year plan over a 4-month discharge?

You might wonder why anyone would choose the longer route. Usually, it's because:

- You have too much equity: You own a home or car that you would lose in a Chapter 7.

- You have high income: You failed the means test but still need debt relief.

- You have "non-dischargeable" debt: You owe back taxes or child support that Chapter 7 can't touch, but Chapter 13 can help you manage.

The Battle of California Exemptions: 703 vs. 704

In California, you have a unique choice that most other states don't offer. You must choose between two "systems" of exemptions to protect your property. This choice is where a bankruptcy lawyer in San Diego, CA, becomes your best asset.

System 1: The Homestead Heavyweight (CCP § 704)

This system is for the homeowners. In 2026, California’s homestead exemption allows you to protect a massive amount of equity: up to approximately $743,000 in many parts of San Diego and California. If you have lived in your home for years and the value has skyrocketed, System 1 ensures you don't lose that roof over your head.

System 2: The Wildcard Wonder (CCP § 703)

If you are a renter or don't have much equity in your home, System 2 is often the winner. It includes a "wildcard" exemption. This is a bucket of money: usually over $30,000: that you can apply to anything. Want to save your tax refund, your fancy mountain bike, and the cash in your checking account? System 2 is usually the way to go.

Notes for Business Owners

If you own a small business in California, your bankruptcy needs are a bit different. A Chapter 7 can effectively shut down a corporation or LLC, while a "personal" Chapter 7 might leave your business assets vulnerable if they aren't properly exempt. If you want to keep the doors of your shop open while handling personal debt, Chapter 13 (or even Chapter 11 for larger entities) might be the safer bet. It allows you to continue operations while managing the debt that is weighing you down.

What will it cost you?

We believe in transparency. For 2026, the court filing fees are $338 for Chapter 7 and $313 for Chapter 13. Beyond the filing fees, the attorney's fees will vary based on how complex your life is. A simple "no-asset" Chapter 7 is very different from a Chapter 13 involving a rental property and three cars.

Don't let the fees scare you. In many cases, the amount of money you save by stopping interest payments and wiping out debt far outweighs the cost of the filing.

Why work with the Law Office of Andrew H. Griffin, III, APC?

You shouldn't have to guess which chapter you need. One is a sprint, the other is a marathon: and we will help you pick the right shoes.

At the Law Office of Andrew H. Griffin, III, APC, we have been serving the San Diego community since 1983. We aren't just lawyers; Andrew Griffin is also a California-licensed real estate broker. This dual expertise is critical when we are discussing your home equity and the 704 exemption system.

We offer:

- 24/7 Accessibility: We know your stress doesn't take the weekend off.

- Text Messaging: You can reach us the way you reach your friends.

- Bilingual Support: We serve our Spanish-speaking community with pride.

- 40+ Years of Experience: We have seen every market shift and law change since the 80s.

Take the first step toward your fresh start

It is normal to feel overwhelmed, but you don't have to stay that way. Whether you need a bankruptcy attorney in San Diegoto stop a foreclosure or an expert to wipe out medical debt, we are ready to guide you.

Contact the Law Office of Andrew H. Griffin, III today for a free consultation. You can call us at 619 853-3009 or reach out through our online contact form. Let’s get you back on your feet.